Stand-up pouches (SUPs) is now one of the fastest growing flexible packaging formats with global demand expected to pass 90 billion units in 2017, according to a newly published report from specialist industry consultants, AMI.

The favourable development of the total supply chain cost of stand-up pouches and their stronger proposition to promote sustainability compared with rigid packaging alternatives will continue to be the key drivers of demand.

“Despite the initial high capital investment in stand-up pouch filling lines, the overall savings on packaging costs in tandem with stand-up pouches’ good environmental profile will continue to keep brand owners interested,” says AMI Consulting Senior Market Analyst Márta Babits. The growth of speciality pouch contract packers has also contributed to driving down costs and expanding interest in SUPs

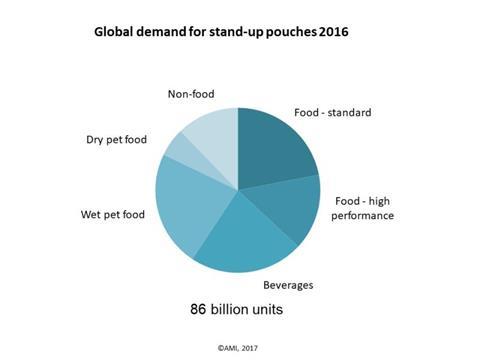

Wet pet food in stand-up pouches is long-established and still the largest segment particularly in developed markets driven by the substitution of cans. The market penetration of beverages has been facilitated by the global market success of Capri Sun, the leading juice drinks brand in stand-up pouches, produced under licence by different bottlers across the world and with a continuously expanding production footprint.

Currently the fastest growth can be seen in the high-performance food category, particularly ready-to-eat baby food and fruit compotes driven by glass jar replacement and growing consumer demand for light weight, safe and convenient packaging for on-the-go consumption. Other segments such as liquid yoghurts are still niche but enjoying double digit growth benefiting from new large scale investments by leading global brand owners.

The market has seen several acquisitions by major flexible packaging converters in recent years and it is expected that consolidation will continue. The largest converters worldwide include Amcor, Mondi, Proampac, Bemis, and Dai Nippon.

AMI Consulting forecasts that demand overall for SUPs will reach 113 billion units by 2021, a CAGR 2016-21 of almost 6%, but growth in some segments will be well above the average. “There are still technology gaps to meet complex customer demands particularly in high-performance applications to balance costs and technical requirements which will provide opportunities for innovative and well organised companies” concluded Márta Babits.