Since the Russian invasion of Ukraine in 2022, the country’s packaging market ‘significantly declined’ in the first year of war – but sectors such as food, paper and cardboard reportedly doubled their volumes in 2023. Valery Krivoshey PhD and Veronika Khalaydzhi PhD IAC of Upakovka outline the key trends and factors influencing the packaging market.

Despite the severe initial shock of the full-scale Russian invasion in 2022, the Ukrainian packaging market has demonstrated extraordinary resilience and adaptive capacity. While most segments experienced significant declines, especially in the first year of the war, key sectors such as food paper and cardboard packaging have shown impressive recovery, doubling their volumes in 2023 compared to 2022.

This recovery, which occurred against a backdrop of hostilities, has been a clear testament to the industry’s ability to adapt, resume operations and meet demand, defying initial assumptions of prolonged stagnation. The war has forced a critical reorientation of supply chains away from traditional partners such as Russia and Belarus towards new sources in the EU and Turkey, underscoring the industry’s resilience.

Key trends shaping the market include a focus on sustainability, innovative packaging materials and packaging, and a shift in consumer preferences towards eco-friendly packaging, which will gain momentum. The market outlook is cautiously optimistic, and the return of the packaging sector to pre-war levels after the conflict will depend on government support programs and international financial assistance.

Market situation in the first year of the Russian invasion

The packaging market is an important artery of the Ukrainian economy, ensuring the functioning and distribution of products of such important sectors as the food industry, pharmaceuticals and consumer goods. Its condition directly reflects economic stability and consumer activity. The “health” of this market is an indicator of the general economic condition, especially the consumer goods, food and beverage sectors.

If the packaging market, especially for such a critically important sector as food, shows signs of recovery and increased production, then this means that the industries it serves are also recovering or maintaining a significant level of activity. Thus, the indicators of the packaging sector serve as an indicator of the viability of the main industries working with consumers, and, accordingly, the overall adaptive capacity and stabilization of the Ukrainian economy in wartime conditions.

The full-scale Russian invasion in 2022 had a devastating impact on the Ukrainian packaging market. From the first days of the war, enterprises located near the front line were directly affected by the fighting. For example, Rubizhanskyi Cardboard and Packaging Plant (Luhansk region) and Dunapak Tavria (Kherson region) were occupied. In February and March 2022, seven cardboard and paper plants were shut down: Papir-Mal (Zhytomyr region), Gofropak (Sumy region), Kharkiv Corrugated Cardboard Plant, ASS-Gofropak, Vostpak (Kharkiv), Mena-Pak (Chernihiv region), and Hermes-T (Chernihiv).

A significant proportion of factories that produced glass containers also stopped in 2022 and resumed operations only in 2023. One of the largest manufacturers of glass containers not only in Ukraine but also in Europe — Vetropack Gostomelsky Glass Plant, a member of the Vetropak group, ceased operations.

Businesses shut down after Russian attacks (as of 2022)

The war has seriously disrupted supply chains and transportation opportunities. Port blockades and air travel bans have forced reliance on less efficient rail and road transport. External factors, such as the Polish farmers’ strike in January 2024, have further exacerbated logistical problems, causing significant delays in deliveries. Energy security has become a major and ongoing problem for businesses across Ukraine, directly affecting production costs and operational stability.

According to experts, as of 2022, the most significant factors that significantly affect the packaging production and consumers of any packaged product are:

- Partial loss of production capacities and markets;

- Logistics complications;

- Reduction in the possibilities of reliable supply of raw materials;

- Increase in energy prices and power supply interruptions;

- Increasing losses of human resources;

- Devaluation of the national currency and inflation;

- Impoverishment of a significant portion of the population;

- A state of chronic stress;

- Forced and voluntary migration.

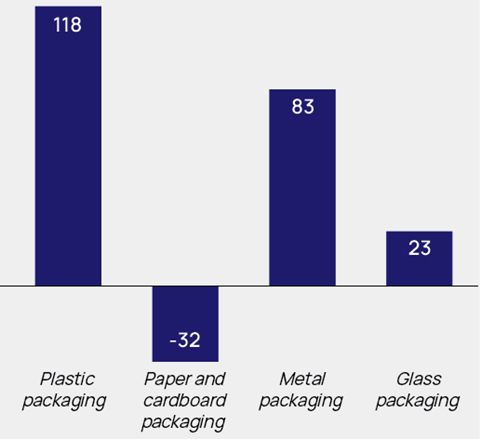

Until 2022, the Ukrainian packaging industry demonstrated its strong development (Fig. 1). However, the war and related problems already in 2022 led to a significant drop in production in almost all groups of packaging compared to 2021 (Fig. 2). The largest reductions were recorded in the production of plastic and metal containers (–51%), cardboard and paper packaging (–44%), corrugated cardboard (–43%), metal corks and lids (–38%), and glass containers (–31%).

Such a sharp initial drop in production in 2022 was a direct result of the physical destruction of packaging enterprises, the occupation of some of them, and critical disruptions in the supply chains of raw materials, energy, and finished products, and not just the general economic downturn. The rapid and widespread reduction in production, as well as specific examples of physical and operational disruptions, are an expression of the direct causal relationship between military operations and the volume of packaging production.

This was not just a decrease in consumer demand, but a fundamental disruption of the ability to produce and transport packaging and packaged products. Already in the first weeks of the war, enterprises located in cities where hostilities took place were stopped, and some were damaged.

This applies to the eastern, southern and northern regions (Kyiv city, Kyiv, Odesa, Kherson, Mykolaiv, Kharkiv, Sumy, Chernihiv, Luhansk and Donetsk regions). There are factories producing cardboard, corrugated cardboard and packaging from them, plastic, glass and aluminum packaging, packaging equipment. Many enterprises did not work due to a shortage of raw materials, spare parts for equipment and the absence of workers who went to defend Ukraine.

In other regions, enterprises tried to work, but some had to reduce capacity. The problem with raw materials became critical for many: cellulose, waste paper, cullet, polyolefin polymers, and polyethylene terephthalate. In addition, curfews, regular long-term air raids, and constant rocket attacks led to reduced working hours and productivity, which complicated logistics.

Fig. 2. % reduction in the production of some types of packaging products in 2022 compared to 2021

The Ukrainian packaging market has always maintained a high dependence on imports of raw materials, especially polymers. A key consequence of the war was the immediate stopping of cooperation with the aggressor countries, Russia and Belarus, which previously supplied up to 15% of the raw materials for food plastic packaging.

This led to a rapid redistribution of import sources, which demonstrates the active strategic decisions and operational flexibility of Ukrainian companies in securing important resources under extreme pressure. They successfully overcame geopolitical changes and logistical challenges to find alternative suppliers, which turned a critical vulnerability into a more diversified and potentially sustainable supply chain.

However, in the first year of full-scale war, imports of some types of finished packaging increased significantly (Fig. 3). For example, imports of plastic packaging increased by 118%, metal packaging by 82.9%, and glass packaging by 23%. This indicates that imports became a crucial mechanism to compensate for disrupted domestic production to meet domestic demand against the backdrop of serious production disruptions caused by the war. When domestic supply was severely constrained but demand for basic goods (requiring packaging) remained, the logical response was to increase imports.

The scale of the increase in imports directly correlates with the significant decline in domestic production of these types of packaging. This indicates that imports were not just a normal business activity, but a vital, adaptive strategy to prevent critical supply shortages in the domestic market, highlighting the flexibility of the industry in redirecting supply chains.

In contrast, imports of paperboard packaging decreased by 32% in 2022, indicating different supply and demand dynamics for this particular packaging, possibly due to internal resilience or demand changes. The main importers are often large consumer goods manufacturers that import packaging for their own production needs. This highlights the closed nature of a large part of the import market.

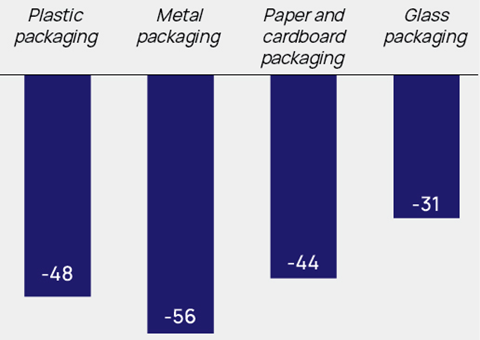

At the same time, the full-scale Russian invasion severely affected the export of Ukrainian packaging, experiencing a significant decline in all types in 2022 (Fig. 4). The largest reduction in exports was for metal packaging (–56.1%). The reduction in exports of plastic packaging was 48%, cardboard and paper packaging — 44%, and glass packaging — 30.8%.

These declines reflect the combined impact of production disruptions, logistical challenges and reduced access to traditional markets. Before the full-scale invasion, Russia and Belarus were significant partners in the plastic packaging segment, accounting for as much as 15% of Ukrainian exports in the first two months of 2022, before the trade suspension.

Now, in the structure of Ukraine’s plastic packaging exports, Poland has taken the largest share (19%), demonstrating a clear shift towards EU markets. For paper and cardboard packaging, EU countries, with Poland as a stable leader, remained the main buyers, indicating a stable, albeit reduced, export channel.

Establishing new, strong trade relations with the EU and other Western countries means a fundamental and, probably, permanent reorientation of Ukraine’s trade geography. This accelerates Ukraine’s economic integration into the European single market and global supply chains, reducing its historical dependence on post-soviet economic blocs. This forced reorientation is a strategic long-term consequence of the war, enhancing Ukraine’s geopolitical and economic security.

Packaging market recovery

Packaging is a product of secondary demand, since its production volumes and development dynamics depend on the state of the main producers of food, beverages and consumer goods. The food industry is the main consumer of packaging materials and packaging, accounting for more than half of all packaging. Compared to developed countries, this share is the largest in Ukraine, since other production sectors are less developed.

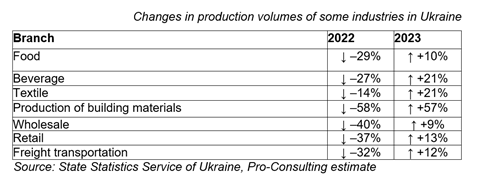

In 2022, the decline in market volumes by the main consumer industries of packaging was almost 35%, but the following year their recovery began - up to 20% depending on the industry. The best dynamics of recovery were shown by national producers of meat and meat products, beverages, confectionery and building materials (shown in the table).

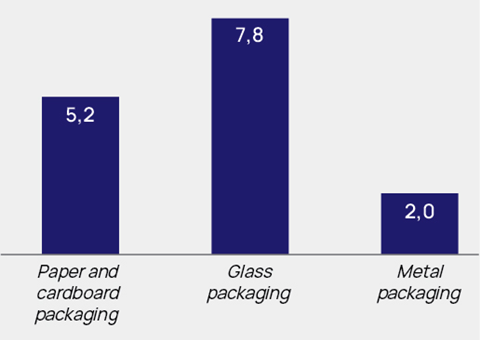

They became like a locomotive in the recovery of packaging, starting in 2023. According to YC Market, in 2022 the paper and cardboard packaging market decreased by 44%, and in 2023 it recovered by 5.2%, the glass market decreased by 38.8%, and in 2023 it had +7.8%; metal packaging — a drop of 44.8% and a recovery of 2% (Fig. 5).

For example, the volume of the market for paper and cardboard packaging for food products, a critically important segment, reached UAH 10 billion. This is double the 2022 level and around 70% of the 2021 level. This rapid recovery, especially for food packaging (a basic necessity), suggests that underlying demand for these products has not disappeared but has been temporarily unmet due to supply-side constraints (e.g., damaged factories, logistical blockades).

It also suggests that the 2022 downturn was primarily a “supply shock” (inability to produce and deliver) rather than a “demand shock” (lack of consumer demand). Once manufacturers were able to resume operations and adapt logistics, latent demand quickly translated into increased production, demonstrating the intrinsic strength of the market and its resilience in meeting basic needs.

Manufacturers of cardboard and paper packaging, such as Kyiv Cardboard and Paper Mill, Trypillya Packaging Plant, and Poninkivska Cardboard and Paper Factory-Ukraine, increased production volumes in the first half of 2023. Thus, Kyiv Cardboard and Paper Mill increased production output by 13.2% compared to the same period of the previous year, which indicates a significant operational recovery.

The plastic packaging market is also adapting to new realities. Many companies have been forced to relocate their facilities, and some, such as Chernihiv manufacturer Plast-Box Ukraine, are planning to restore a destroyed plant.

The glass packaging market has undergone significant changes. The shutdown of one of the largest players, Vetropack Gostomel Glass Plant, has significantly affected the market landscape. On the one hand, this has created a shortage, and on the other hand, it has stimulated demand for products from other domestic manufacturers and contributed to the reorientation of consumers to local suppliers. There is a decline in demand for decorative packaging, while demand for standard canning jars is increasing.

Information on the metal packaging market is the most fragmentary. The available data relates mainly to the metallurgical industry as a whole, and not specifically to the production of containers.

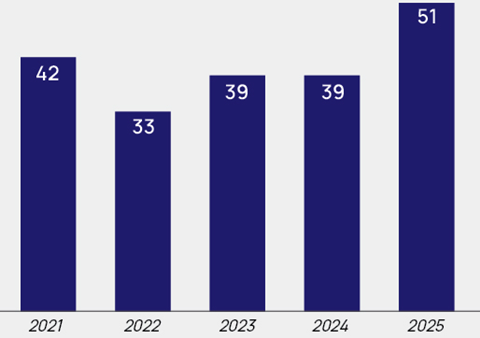

In 2023, there was an increase in the consumption of plastic-coated metal, which can serve as an indirect indicator of demand in the packaging industry. The share of Ukrainian manufacturers in this segment has increased, which indicates gradual import substitution. The positive recovery of the Ukrainian packaging market is indirectly confirmed by the increase in the number of packaging samples that participated in the Ukrainian Packing Star competition in 2023-2025 compared to 2022 (Fig. 6).

In general, the packaging industry of Ukraine in 2023-2025 is going through a difficult stage of transformation. Despite the loss of part of its production capacity, the market demonstrates the ability to adapt, reorient to new sales markets and gradually restore production volumes. Further development of the industry will largely depend on the military-political situation in the country and state support for manufacturers.

Packaging on the line of fire

In the context of Russia’s full-scale war against Ukraine, packaging for food and medical supplies for the military has ceased to be just containers. It has become a critically important element of logistics, survival, and combat capability, requiring maximum functionality, reliability, and adaptability to extreme field conditions — from flexible retort packages for borscht to airtight pouches for individual first aid kits.

The main requirements for food packaging at the front line is ensuring long-term storage without special conditions and protection from moisture, dirt, and mechanical damage, as well as ease of use.

The packaging must be airtight and durable. It must withstand off-road transportation, falls and weather conditions, and protect the contents from bacteria, dust and chemical contamination. Its portion size and lightness are important. Individual food rations (dry rations) are designed for one meal, which allows soldiers not to carry excess weight.

There has been a significant shift away from heavy and inconvenient metal cans. The packaging must be easy to open without additional tools and warm up. In combat conditions, every second counts. Modern solutions, such as flameless chemical heaters that come with dry rations, allow you to heat food without fire, which is critical for masking positions.

The biggest breakthrough was the mass introduction of retort packages — multilayer flexible packaging in which ready-made dishes (borscht, porridge with meat, stew) can be sterilized and stored for up to two years without refrigeration. Ukrainian manufacturers, in particular the Kharkiv company Aris, quickly adapted their technologies for military needs, producing Naidok retort packages for packaging bograch, cabbage rolls and other traditional Ukrainian dishes (Fig. 7).

Volunteer initiatives played a significant role in this process. Often, it was they, in collaboration with manufacturers, who created products that met the needs of the military. An example is the design of labels developed for packaging three types of stew (developed by the TCD company), with the patriotic inscription “With love for the Armed Forces of Ukraine”, which is designed to raise fighting spirit.

Packaging for medical and tactical medical equipment must provide instant access to the contents, maintain its sterility and protect it from any external influences. An individual military modern first aid kit must comply with NATO standards and TCCC (Tactical Combat Casualty Care) protocols.

Its outer packaging is made of moisture-proof durable materials in protective colours. The design provides a fastening system for convenient placement on equipment and the ability to open it with one hand. The contents of the first aid kit (tourniquets, bandages, hemostatics, occlusive stickers) are securely fixed with elastic bands and placed in pockets for quick access.

Each medical device has its own sealed and sterile packaging that is easily torn. The wounded person’s card, which is a mandatory element of the first aid kit, is made of waterproof material, and the marker for recording the time of applying the tourniquet is permanent. Tableted drugs are packed in rigid blisters or containers.

Ukrainian manufacturers, such as Medipak Ukraine, provide medical stabilization points with special packages and rolls for sterilizing instruments, which is critically important for maintaining sanitary standards in field hospitals. Volunteer organizations such as Razom for Ukraine and the Leleka Foundation made a huge contribution to providing the military with quality first aid kits.

They massively purchased certified components, assembled the kits and delivered them to the front. At the same time, one of the problems at the beginning of the invasion was the large number of uncertified and low-quality medical supplies arriving as humanitarian aid, which created risks for the lives of the wounded.

Finally

Thus, the war became a catalyst for rapid and effective changes in military packaging, demonstrating the synergy between government agencies, private manufacturers, and a powerful volunteer movement. Modern packaging not only preserves, but also directly helps save lives on the front lines.

The outlook for the packaging market is cautiously optimistic. The expected return of Ukraine’s economy to pre-war levels after the end of the war, driven by large-scale reconstruction projects, will create significant demand for packaging. This, combined with global growth trends in the packaging market and Ukraine’s aspirations for European integration, positions the industry not just for recovery, but for modernization and a potential transition to advanced, consumer-focused, sustainable solutions. As a result, the Ukrainian packaging market will emerge from the war stronger, more adaptable and future-oriented than ever before.

If you liked this story, you might also enjoy:

The ultimate guide to packaging innovation in 2026

Packaging and Packaging Waste Regulation: what to know in 2026

Everything you need to know about global packaging sustainability regulation

No comments yet