With the premium water market forecast to grow to $70bn this year globally, a new study by automated market research technology company, ZappiStore, explores packaging messaging in the premium and bottled water market.

The study reveals that several premium water brands, including the recent offering Lifewtr from PepsiCo, may face a long journey establishing their water messaging compared to brands that have more familiarity in the market.

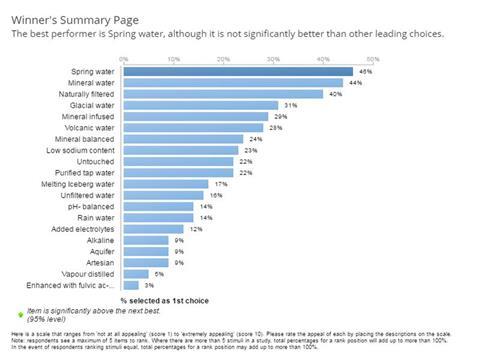

ZappiStore tested the messaging on the packaging of 20 premium and bottled water brands with 1,000 nationally representative respondents in the US and UK. It found that packaging claims for many of the newer premium water brands, such as Coca-Cola’s SmartWater, Pepsico’s Lifewtr, Voss, and Fiji Water generally score lower on purchase intent and believability metrics than more established spring and mineral waters.

Key findings:

• Purchase intent in the UK and US was topped by ‘mineral water’ and ‘spring water’ respectively. Purchase is based on the question ‘how likely are you to purchase the product’ and calculated as a ten point scale, with ten being definitely intend to purchase.

• In the UK, the top five claims based on purchase intent are all featured on the packaging of established brands such as Evian, Volvic, Perrier, San Pellegrino, and Buxton.

• In the US, common claims from newer premium water providers generally score better for purchase intent than the UK. ‘Artesian sourced’ water (Voss, Fiji Water, Hawaii Water) scores a 6.7 on purchase intent in the US, but only a 4.9 in the UK. Whereas ‘glacial water’ (Isklar, Clear Alaskan) is ranked 3rd in the US with a 7.2 purchase intent score, but is ranked 7 by UK respondents with a 6.1 score.

• ‘Purified tap water’ produced a far stronger purchase intent than many of the claims offered by premium water providers, such as ‘vapour distilled’ (SmartWater), and ‘unfiltered water’ (Voss). ‘Purified tap water’ was rated at the same purchase intent as Pepsico’s Lifwtr claim of being ‘ph-balanced’.

• The top drivers for purchase intent of bottled water are: ‘refreshing’, ‘top quality’, ‘good for me’, ‘easy to understand’.

The survey indicates the amount of time in market and familiarity, have a significant impact on purchase intent in both markets. In the UK claims from established and traditional bottled water providers from the UK and Europe, such as ‘mineral water’, ‘spring water’, ‘low sodium content’, and ‘naturally filtered’, all score higher than claims from newer entries into the water market. Claims such as ‘artesian’ or ‘vapour distilled’ and ‘enriched with fulvic acid’ do not garner the same purchase intent in consumers. However out of the 20 claims ZappiStore assessed, the term ‘volcanic’ water, which is used on the packaging for the UK and European mainstay brand Volvic, ranks 4th for purchase intent in the UK, but drops to 17th in the US, where the brand is less established. Alternatively claims from Voss, Fiji water, Hawaii water, and Smart Water such as; ‘artesian sourced’, ‘aquifer water’, and ‘added electrolytes’ score higher for purchase intent in the US, a market where these premium water suppliers have been established for longer.

The ZappiStore study found that the top emotional attributes for purchase intent for consumers in both markets are ‘refreshing’, ‘top quality’, ‘good for me’, ‘easy to understand’. For Coca-Cola’s SmartWater, claims such as ‘naturally filtered’ indexed well in the UK for ‘easy to understand’ (41% of respondents associated the claim with this attribute), followed by ‘good for me’ (38%), ‘refreshing’ (37%), ‘environmentally friendly’ (37%). Whereas the PEPSICO Lifewtr claim of being ‘pH-balanced’, scored lower across all key drivers; 29% for ‘good for me’, 21% for ‘top quality’ and 19% ‘easy to understand’.

The study also found that claims which score lowest for purchase intent are generally product claims that consumers find confusing. ‘Enhanced with fulvic acid’, a claim from niche water provider Blk Water, was found to be confusing by 51% in the US and 41% in the UK, whereas ‘vapour distilled’, a key claim of SmartWater was found to be confusing by 35% in the US and 29% in the UK.

The study also found that Dasani’s purified tap water ranks at 11 in the UK and 9 in the US for purchase intent. This most basic of claims beat others such as ‘vapour distilled’,’ iceberg water’, and ‘alkaline infused’, in both markets. This demonstrates that a high attribute score for ‘easy to understand’ (40% in the US and 37% in the UK) are claims that resonate with consumers more, even if it seems on paper they may seem to be less glamorous and innovative than other premium water claims.

The ZappiStore water packaging claims study shows that time in market is a key driver to purchase intent and understanding of claims. But as a market due to grow to at $70 billion this year, it still offers a huge opportunity to brands. However in order to be competitive in such a crowded market, brands need to keep packaging claims easy to understand, and communicate a refreshing and healthy drinking experience. Those with more niche claims should be prepared for the long haul and increased marketing investment to make a significant impact and look to educate consumers on the benefits of the health and source claims they currently finding confusing.

Methodology

The ZappiStore bottled water study surveyed a nationally representative sample of 500 respondents in the UK and 500 in the US through their proprietary ‘Favour it’ tool.